Disruptive innovation in the energy sector – definition & application to renewables

Nowadays, one can easily be under the impression that all business models that provide the foundation for most industries are fundamentally challenged by disruptive innovations. If we take a look at the energy sector, many different innovations are supposed to be disruptive: renewables, electric vehicles, battery storage, smart metering and blockchain are just a few examples of technologies that are commonly described as disruptive innovations for energy utilities. However, according to Clayton Christensen (Harvard University), the concept of disruption is not understood by the majority of those who talk about it (see Christensen, Raynor & McDonald (2015) for details). The problem here lies within the lack of definition of disruption, or to be more precise, the lack of application of the definition of disruptive innovation. This seems to be even more surprising as the term “disruptive innovation” has already been defined by Christensen in 1997 in his book The Innovator’s Dilemma. Though this definition provides just one view out of many on disruption, it is the most sophisticated theoretical approach so far, at least to our knowledge.

Based on Christensen’s definition of disruption, only very few technologies actually qualify as being disruptive. To clarify we will give Christensen’s definition and provide one example of a disruptive innovation for energy incumbents in Germany.

The definition of disruptive innovations by Clayton Christensen

Basically, Christensen defines disruption as a process in which a new market entrant, e.g. a startup, enters a market that is currently dominated by incumbents and successfully gains significant market shares, even though the new market entrant has far less resources than the incumbents. However, Christensen’s understanding of disruption goes deeper as he made a very interesting observation in different industries in the 80s and 90s: Even though incumbents had a market dominant position and were managed very well, they struggled to adapt to new products which eventually took away their customers and thereby their revenues. Christensen made this observation in the context of mainframe computers vs. personnel computers as well as in other industries like cellular phones vs. fixed line phones. By analyzing these developments, Christensen identified that disruptive technologies do not take the incumbents’ market share by surprise, but that the incumbents actually face the upcoming threat but decide to ignore it, primarily, as the direct impact on the current revenue is not yet visible. How come that top managers see it coming that a technology eventually will take over their market share and thereby reduce their revenues, and still do nothing about it?

Focus on premium products with high revenues

Christensen claims that the primary reason for this behavior lies in the fact that large companies tend to focus on their premium customers and premium products with the highest revenue and market share. As a consequence of this, they focus their innovation processes on the improvement of these premium products, adding new features to it to fulfill the premium customer’s expectations. The idea is simple: If you have a successful product, try to improve it to increase revenues. However, increasing the functionality of a product eventually results in a product that exceeds the customers’ requirements, at least of the average mass customer. While a more advanced product might be interesting for premium customers, the average customer might not require the new product specifications, i.e. is not willing to pay for the premium product. This is the first step towards disruption: Over-equipped premium products that exceed the needs of the average mass customers.

Insufficient attention is paid to the low-end or new market

The second step towards disruption then is that the successful incumbent solely focuses on the high-end market with high revenues from its premium products, while the company ignores the low-end (or new) market where new products with less revenues and only a small customer base are located. In contrast to a Return-on-investment-perspective (ROI), an investment in the low-end (or new) market conflicts with this principle as only low margins and small profits can be expected in the low-end (or new) market. Incumbents, in their risk-adverse nature, do not invest in such markets due to information deficiency about the market opportunity or simply because they do not want to cannibalize the sales of their high-end products. While this seems to be the right decision from a short-term and revenue-based perspective, it opens the door for new market entrants that can gain market shares in the low-end.

Alternatively, the second step involves the development of a new market, meaning that a new market player has a product or service that transforms non-consumers into consumers. In this case, the primary advantage of the new market entrant is a new feature that fulfills a specific customer need (the customer hereby might not even be aware of this need until it is offered to him or her).

New products with lower ROI conquer mass-market

This introduces the third step of the disruption process: A new market entrant focuses on the low-end market or a new market with a new product that at first glace is less interesting from an ROI perspective and from the perspective of the average mass-customer as well. Therefore, the incumbent does not bother much about the new competitor. However, the new market entrant can make use of its position in the low-end market to further develop its product towards the mass-customers needs. Many disruptive innovations actually start by providing one specific feature that is not provided by the incumbents product. Thereby, they offer a cheaper product that addresses a specific need, but that is overall less convenient or less advanced than the incumbents’ premium product. However, using this specific feature as a basis, the new market entrant develops its product to fulfill the basic requirements of the early adopters. Based on the niche of early adopters the new market party further develops its product to fulfil the expectations, e.g. with respect to quality, of the average mass-market customer. Then, the point is reached where the average mass market customer switches from the expensive premium product that provides features the average user does not require, to the cheaper product from the new market entrant that has less features, but that provides the specific application that safeguarded its success in the low-end market. Now, the incumbents lose market shares against the new product and eventually, the mass-market switches towards the new product: voilà, disruption occurs.

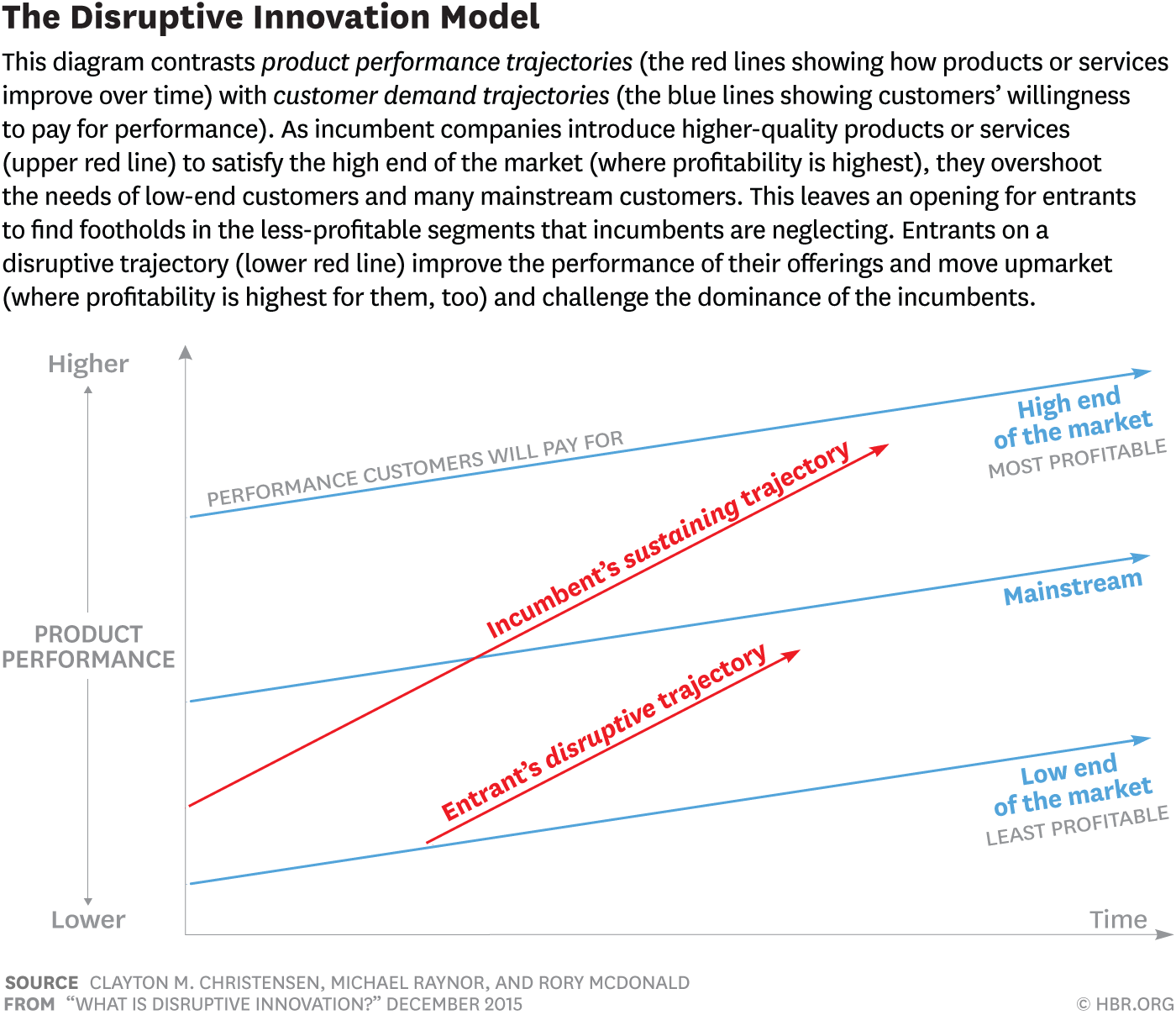

Figure 1 sums up the process of disruption by showing the difference between the incumbents’ strategy to sustain revenues from premium products vs. low-end products that gradually disrupt the incumbents business model by gaining shares in the mass market.

Figure 1: The Disruptive Innovation Model (source: Christensen, Raynor & McDonald (2015))

Against this backset, Christensen says that disruptive innovations are

“typically simpler, cheaper, smaller and frequently more convenient to use” than the products offered by incumbents. (Christensen, 1997:10)

Distributed generation from renewables as a good example for disruptive innovation in the energy sector

Now, to give you one example of a disruptive innovation in the energy sector, let us take a look at distributed generation from renewables in Germany by distracting three different criteria from Christensen’s definition of disruptive innovations.

Low-end/ new market & Return-on-investment

What we’ve seen in Germany is that incumbent utilities did not actively invest significant capital in renewables till 2016. Rather, the largest utilities (E.on, RWE, ENBW and Vattenfall) focused their generation business on conventional generation from fossil fuels and nuclear, as these power plants provided high revenues till 2010. Especially in the time period between 1990 and 2010 incumbent utilities did not invest much in renewables as the revenues from their premium products (conventional power plants) were much higher. Renewables, on the other hand, did not provide such high revenues, at least till the year 2000 when the feed-in tariff (FIT) scheme was introduced that secured a stable ROI for renewable generators over a period of 20 years of operation. Even after the introduction of the FIT utilities hesitated to invest much capital into renewables due to other reasons, e.g. the size of the RES projects. Till 2005, RES projects were rather small, with investments far below the common investment budgets the energy industry was used to. Furthermore, renewables so far were not able to provide ancillary services to the networks, like voltage or frequency control, which are services that conventional power plants provide to generate additional income for the utilities. Taking all these aspects together it becomes obvious that renewables entered the market at the low-end with low revenues. At the same time, decentralized generation from renewables opened a new market as well as it was no longer limited to small-scale hydro generators. Especially with photovoltaic power plants that can be constructed on any roof or even on balconies, renewables opened a new market segment in contrast to the central generation units that required huge investments and involved very high risks.

From low-end and new market to mass-market based on a new feature

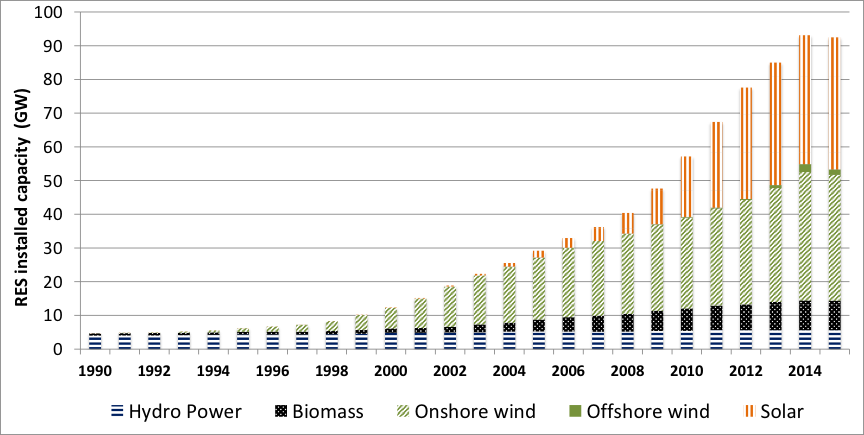

While incumbents did not invest in renewable energy resources, others did. Especially private households, farmers and energy cooperatives started investing in renewables due to two reasons: First, with the FIT, the ROI was sufficient for private investors. Second, renewables provided a new key feature the established products did not provide: decentralized power generation with zero CO2-emissions (apart from the emissions related to the production process). Together, the attractive ROI, the potential to reduce CO2-footprints and the decentralized character drove the market share of renewables quite fast in Germany. Figure 2 shows how renewables in Germany grew from 1990 till 2015.

Figure 2: Development of renewables in Germany from 1990 till 2015 (source: Brunekreeft, Buchmann & Meyer, 2016)

Still, renewables did not enter the mass market right away, but over a period of about 15 years. Especially efficiency, quality and reliability needed improvement to fulfill the mass market’s needs. Ever since renewables are part of the German mass market, investment have been dominated by private households and farmers who owned 46% of the 73GW renewable electricity supply in Germany in 2012, while all incumbents (not just the big four, but all) owned only 12%.

Reduce revenue of premium products

Currently, we can observe that renewables push conventional power plants out of the market. This happens in different markets, most remarkably in Germany, California and Texas. In these markets, renewables shift the merit order of the market dispatch to the right, reducing the average wholesale electricity price and reducing the full-load hours of conventional power plants, especially gas-fired power plants. This effect, called the merit-order effect, is illustrated for the case of Texas in the following graphic.

Figure 3: The Merit Order Effect in Texas

An illustration of the electricity market bid stack for the ERCOT grid in Texas. Generators line up left to right from the lowest cost to highest cost every five minutes. As demand changes throughout the day, the ‘marginal generator,’ or the last power plant called to provide power, sets the price that every plant providing power (left of the vertical black line) is paid. Power plants to the right of the line are not dispatched and thus do not receive payment in an energy-only market. (NG CC = Natural Gas Combined Cycle; NG Other = NG boilers and combustion turbines). University of Texas at Austin, CC BY

Obviously, regulation and incentive schemes for renewables have significantly influenced this market development. Utilities also have had the chance to invest in renewables, but did not take it. Besides the aspect that the ROI of conventional power plants was or at least seemed to be higher from the utilities perspective (which is not the case anymore), the fear of self-cannibalization was another reason not to invest in renewables. As we have discussed in this post incumbents did not invest in renewables to protect the market share and revenue of their conventional power plants. As we can see in figure 2, the revenue of conventional power plants, especially costly gas-fired power plants, is reduced by increasing shares of renewables, as the average wholesale price falls with increasing shares of renewables.

Summing up, renewables fulfill Christensen’s definition of disruptive innovation quite well. Now, what can utilities do to adapt to the disruption?

How Energy Incumbents can react to disruptive innovations

In his analysis Christensen points out that there are several strategies how incumbents can address disruptive innovations. Separation of business units is one approach proposed by Christensen. Basically, the idea is to start a new company that becomes active in the field of the disruption, in our case investment in renewables. It is very important according to Christensen that the innovation is not addressed in a separated unit within the company, but in a separated company where a different culture and vision can be enacted. This is exactly what Eon and RWE did in 2016: They separated the renewable business from conventional generation. Whether this was still in time or too late will become evident within the next decade (see this post for details on this strategy). However, the next potential disruption is currently underway: Blockchain. We will discuss whether blockchain qualifies as a disruptive innovation for the energy sector in our next post. Stay tuned!

Are distribution network operators in Europe threatened by a potential application of blockchain technology in the energy sector? This seems to be the pressing question that was at least partially the motivation for a recent report on blockchain in the energy sector by eurelectric, which is the European association of the distribution grid operators. From our perspective, this report reads like an attempt by the industry to reassure itself that its core business model – asset ownership and operation of the electricity networks – is not threatened by blockchain. While this might be true for asset ownership, this is different in the case of network operation.