10 years since the global financial crisis

We reflect on how the superyacht market has changed since the beginning of the global financial crisis in 2007…

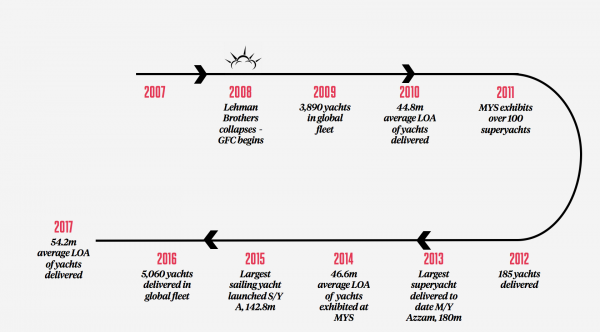

On 15 September 2008, Lehman Brothers, once the fourth-largest private investment bank in the United States, collapsed as it filed for Chapter 11 bankruptcy. And what followed was the worst financial crisis since the Great Depression of the 1930s. The shockwaves of this financial crisis rippled throughout the world and had a profoundly negative effect on many industries, not least the superyacht market.

This year’s Monaco Yacht Show will be the 10th show since the collapse of Lehman Brothers, and 2017 represents 10 years since the subprime mortgage crisis, characterised by the collapse of Northern Rock in the UK, set the wheels in motion for the global financial crisis in 2017.

The housing bubble that was created in the US as a result of the subprime mortgage crisis was not the only bubble that was created due to the availability of credit at the time. According to The Superyacht Annual Report: New Build 2017, in 2007 and 2008 there were 269 and 240 new orders respectively, in 2009 this figure fell sharply to 112. This represents a 53% decline in new business, globally, in just 12 months.

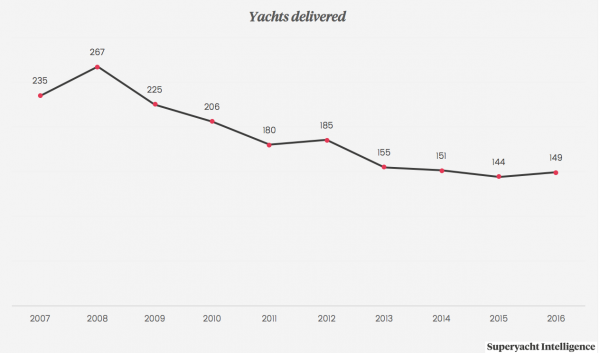

New build deliveries remained relatively buoyant at the time, due in large part, to the number of vessels that had already been paid for and required finishing. However, from 267 deliveries in 2008, the new build market began a steady decline, characterised by the residual effect of the collapse in orders, towards 144 deliveries by 2015.

Since the global financial crisis, the superyacht market has entered a period of realism, consolidation, professionalism and significant change. Whether that be the sudden disappearance of a number of opportunistic and financially unstable yards, the rise to prominence of the refit market, the merging of superyachting superpowers, the changing attitudes of ultra-high-net-worth individuals or the growth in average size of superyachts.

The halcyon days of the mid-2000s and the subsequent dose of realism that followed them played perfectly into the hands of one market sector in particular. When money had been free flowing and financial outlooks incredibly positive, the refit market was widely viewed as being supportive in its role.

In the post-2008 era, albeit slower than before, the global superyacht fleet continued to grow apace, averaging 174.4 deliveries a year from 2009 to 2016. Quality refit infrastructure, however, did not develop at the same speed.

While, undeniably, there has been a host of refit infrastructure developments over the last 10 years, these developments do not account for the 1,897 superyachts that were delivered during this period. As such, competition for premium refit slots during winter has risen, with the quality yards, and even some of the second-tier yards, frequently being booked up a year or more in advance. Moreover, refit, more so than it was before, is now seen as a genuine mechanism for cost saving – a genuine alternative to commissioning a new build, as well as a means of retaining value, should the owner wish to brave a second-hand market saturated with poor-quality vessels.

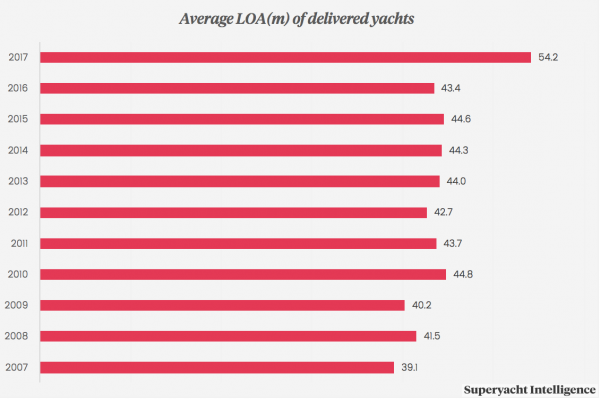

Since the collapse of the markets in 2008, delivery figures fell until 2016, when, for the first time since 2012, the market grew. However, throughout the 10-year period since the crash, superyachts have continued to grow in size. Seven of the top 10 largest superyachts in the world, and 13 of the top 20 largest superyachts, were all built post-2008, and this includes the worldest longest yacht M/Y Azzam (180.61m) and the world’s largest yacht in terms of gross tonnage, M/Y Dilbar (15,917gt).

Change has not only been driven by financial trepidation. Since 2008 there have been great leaps forward in the technology that is available on board superyachts, from AV and IT integration to hybrid propulsion technology, and the whims and wishes of contemporary owners have evolved with technology, developments in design and the possibilities that today’s superyachts afford. Such have been the steps forward in technology that the explorer yacht has grown to prominence. However, the dawn of the explorer vessel has also been a reflection of UHNWIs desiring to maximise the use of their assets beyond the well-trodden grounds of the French Riviera and other superyachting stalwarts.

Any discussion relating to how the industry has changed over the last 10-years would be incomplete without a passing reference to the regulatory and legislative changes that have occurred over this period. Since 2008 the Passenger Yacht Code, Bribery Act, the third Large Yacht Code, MLC, New Insurance Act, Ballast Water Management Convention, Polar Code, STCW Manilla Amendments and Common Reporting Standard have all been introduced, as well as amendments made to the Matriculation Tax in Spain, the French Commercial Exemption, the introduction of the Marshall Islands Yacht Engaged in Trade scheme and a host of fiscal changes in France, the list goes on. And, while many still bemoan the increasingly regulatory environment that the superyacht market finds itself in, few would argue that fiscal developments, codes and various IMO initiatives are not, in many ways, just and for the betterment of the industry as a whole.

The superyacht market still faces tough years ahead. While the new build sector has consolidated by cutting the wheat from the chaff – beginning the long road to recovery, the service industry has boomed and, for the first time, generated more profit in 2016 than the new build sector. Secondary and tertiary sector growth will form a major part of the industyr’s growth strategy moving forward. The recent acquisition of Global Yachting Group by Lonsdale Capital Partners and its subsequent appearance on the London Stock Exchange attests to this.

However, as investors begin to understand the profitability of the superyacht market, disruptive technologies and enterprises will also begin to take on new significance. Those businesses that are content with current models, may find their market shares beginning to diminish if they fail to embrace progress. Equally, the industry must look towards emerging markets and alternative models in order to cater for tomorrow’s superyacht owners and expand the size of the market as a whole.

At The Superyacht Forum 2017, we will be exploring how the market will change over the next 10 years. Join The Superyacht Group Team from 13-16 November in Amsterdam by clicking here.

Click here to become part of The Superyacht Group community, and join us in our mission to make this industry accessible to all, and prosperous for the long-term. We are offering access to the superyacht industry’s most comprehensive and longstanding archive of business-critical information, as well as a comprehensive, real-time superyacht fleet database, for just £10 per month, because we are One Industry with One Mission. Sign up here.

Related news

Careful what you wish for

Disruption is increasingly becoming lauded as the solution to a great many problems. But, is disruption necessarily a force for good?

Technology

The cost of superyacht rigs

Rig manufacturers debunk the notion that there is a typical cost for a superyacht rig package

Technology