Mortgage brokers face multiple challenges as bull market ends

Mortgage brokers are being pounded by slower lending, regulatory headaches, management changes, humiliating royal commission disclosures and some very public spats with their major paymasters, the big four banks.

The share price of listed brokerages are also being battered as investors grow increasingly nervous about whether it's a cyclical downturn or the beginning of systemic change imposed by new technology, a repositioning by major banks and over-zealous regulators.

Global investment banks, such as Morgan Stanley, warn that credit, economic and market conditions are the worst for 30 years, which is when the ground-breaking Campbell Report opened the door for specialist mortgage advisers as an alternative to banks and other lenders.

Mortgage brokers facing multiple challenges. Courtney Keating

Since then broking has evolved from a cottage industry into a powerhouse of more than 6800 businesses, as median property prices in Melbourne and Sydney increased tenfold.

Brokers account for about 53 per cent of deals – and much more amongst smaller lenders with minuscule branch networks – and more than $2 billion in annual commissions.

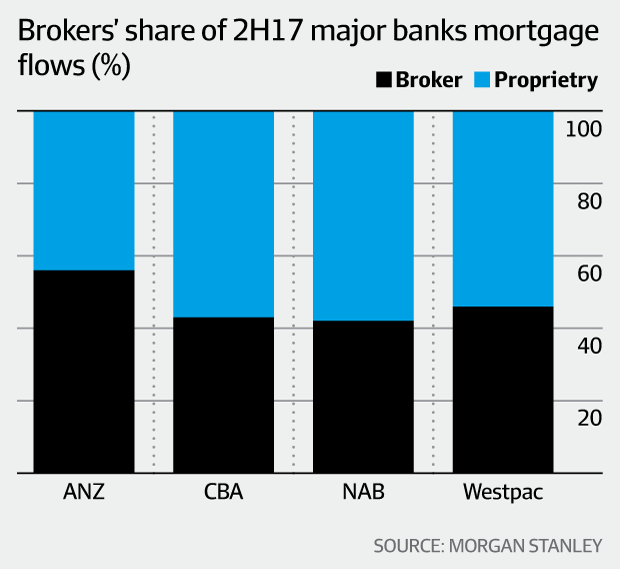

Major banks' market share increased from about 79 per cent to 92 per cent in the five years following 2007's global financial crisis. It has since estimated to have slipped back to about 36 per cent because brokers encourage more competition.

But probes by the Productivity Commission, ASIC, industry groups, other prudential regulators and the current royal commission into financial services are souring relationships with lenders and challenging commission payments.

A mortgage broker who arranges borrower finance will receive an average upfront broking commission from lenders of about 0.6 per cent of the loan value and a trailing commission of just under 0.2 per cent of the loan outstanding per year over the life of the loan, according to the Australian Productivity Commission.

Commission flows slowing

That amounts to a mortgage advisory fee of about $6000 for the mortgage of an average loan of about $357,000.

There can also be lucrative commissions by developers keen to clear stock.

But commission flows are slowing as the number and value of weekend auctions in Melbourne and Sydney, which is largely considered to be a key measure of activity, continues to cool and slows growth, lower profits and reduces the number of new brokers entering the industry.

Some of that slack will be taken up as terms on popular interest-only loans expire and borrowers are forced to reconsider their options, which for most will mean principal and interest.

Lenders are also recruiting brokers to advise on business loans.

But brokers are also being whacked by new digital technologies reshaping every aspect of the industry, cutting costs, squeezing margins on traditional ticket clipping from conveyancing to arranging mortgages.

New generation technologies are linking borrowers to brokers, lenders or both.

For example, new entrants such as Tic:Toc Home Loans are grabbing market share by digitising every step in property buying to reduce the time needed to approve a loan from 22 days to 22 minutes. They also take a smaller commission.

Share prices struggle

The prospect of a federal Labor government by the end of next year and threatened curbs on negative gearing will diminish weakening demand for investment properties.

The share price of Australian Finance Group, which dominates the sector with about 24 per cent market share, has slipped by about 23 per cent in the past six weeks. AFG's competition index shows non-major lenders account for more than one in three loans.

Commonwealth Bank of Australia with 14 per cent market share is facing legal and regulatory issues across most retail operations.

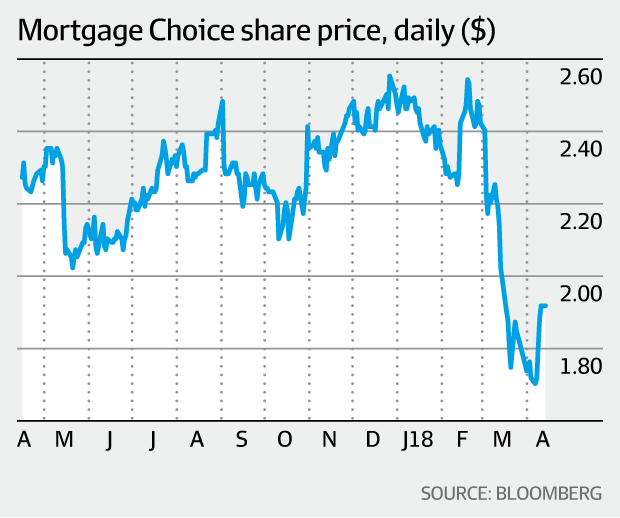

Mortgage Choice, whose share price has plunged by nearly one-third in the past month, is a distant third with 8 per cent.

Its share price has been rattled by the sudden departure of mercurial chief executive John Flavell and replacement by his ex-chief financial officer, Susan Mitchell, who was lured back to the top job after quitting a month previously.

A debate about whether mortgages are a "commodity", like a utility bill, or a "service", requiring advice from a specialist, is generating a lot of heat amongst brokers.

Proponents of a "service" claim that brokers, like financial advisers, provide expert advice and help clients navigate their way around some 30,000 different loan products.

Brokers argue they offer their client services for "free" and earn income from an upfront commission from the lender of about 0.65 per cent of the loan's value and monthly trailing commission of 0.15 per cent.

Battle with banks

This is being fiercely debated by ASIC, the Sedgwick Report on banking remuneration, the Combined Industry Forum, Productivity Commission and dramatically played out before the royal commission in banking practices.

Detailed public examination of the misconduct of former Aussie Home Loans brokers and how the problems were handled has triggered astonishing claims by brokers that they are being used as "human shields" to divert attention from banks.

Brokers were further outraged by Westpac CEO Brian Hartzer's suggestion of a service fee for recommending mortgages because of fears it will tip the balance back in favour of branch-based lending.

CBA is already tightening its qualification standards for new mortgage brokers, toughening scrutiny of its existing network of brokers, which account for about 43 per cent of mortgage flows, and attempting to put more business through its nationwide branch network.

Banks and brokers are bracing for more uncomfortable disclosures at the next round of the royal commission.

Both sides are going to have to give some ground to appease public concern and regulators.

The outcome from all the inquiries is heading toward some form of expectation that brokers' primary focus will need to be on their customers, even though the precise wording of a general fiduciary duty will take time to resolve.

Lenders are already moving toward toughening of how brokers set out applicants' living expenses and income, which has been another source of embarrassing exposure by the royal commission.

For example, ANZ and Westpac Group are requiring brokers to submit borrowers to detailed questioning about their loans, income and future capacity to meet repayments.

Structures 'not broken'

Soft dollar benefits, which cover anything other than a cash commission or direct client fee, are likely to be ruled out.

Some concessions are likely over commission structures.

AFG argues existing structures are "not broken" and enables all borrowers the option of dealing directly with their chosen lender.

But the Productivity Commission and royal commission are questioning whether borrowers should pay a fee to brokers rather than higher interest payments to lenders.

Royal commissioner Kenneth Hayne has even questioned whether brokers did more work on a larger loan than a smaller to justify a bigger upfront commission.

The debate will continue but brokers are pushing for a deal that retains existing payments but improves transparency and accountability on commissions, where loans are written, and the interest rates.

A new model is also likely that avoids financial incentives encouraging consumers to borrow more than they need, or will use.

The Productivity Commission questioned whether trailing commissions, which are paid each year of the loan's term, should be abolished.

Brokers are adamant they should remain. But a workable compromise will likely result in closer scrutiny what they do to justify the payment.

A combination of more onerous capital rules for lenders, tightening lending standards, higher mortgage rates and credit rationing are ending the mortgage bull market.

Expect more pressure on listed brokages' share prices as housing growth and returns slow.

Subscribe to gift this article

Gift 5 articles to anyone you choose each month when you subscribe.

Subscribe nowAlready a subscriber?

Introducing your Newsfeed

Follow the topics, people and companies that matter to you.

Find out moreRead More

Latest In Property

Fetching latest articles