Americans spent over $500 billion last year online, up 15 percent from the previous year, according to a recent industry study. If the sector keeps growing at a similar clip, e-commerce, in less than four years, will be a trillion-dollar business.

Dwell on that for a moment.

SEE ALSO: Amazon Is Now Offering a Credit Card to Customers With Bad Credit

Online shopping, which literally did not exist 20 years ago, now accounts for one out of every seven dollars spent by Americans on retail.

Of course, when e-commerce numbers like these come out, the dominant narrative is usually about who has the biggest piece of this ever-expanding pie (hint: it starts with an ‘a’, ends in an ‘n’ and is named after a South American jungle). But oftentimes, lost in the trees of this gargantuan XXL market is the story of the payment enablers that make it all possible—a cohort that has changed surprisingly very little since the early days of dial-up internet. The payments tools available to online shoppers in today’s marketplace are still fundamentally the same services that were being offered to Diners Club customers back in the 1980s.

Today, one out of every three dollars spent online is charged to a traditional credit card—a number that jumps to one out of every two dollars when including spending with eWallets, like Apple Wallet, Samsung Pa, and Google Pay, which are essentially nothing more than secure digital purses linked to credit cards and charge cards like Visa and American Express.

But all of that is changing; experts believe that a number of new, alternative e-commerce payment platforms are going to shake up the online payments industry, playing an increasingly dominant role in the sector—and just as annual U.S. e-commerce spend surges towards that trillion-dollar mark.

Globally, there are myriad payments practices that are proliferating to meet the specific needs of local markets. From new features being rolled out on PayPal to peer-to-peer money transfer apps like Venmo to China’s WeChat, there are an increasingly diverse number of ways to pay beyond the standard Visa or Amex. But many analysts believe that the biggest disruptors in the current payment system will be a host of companies that play in the so-called “post-pay” arena. These innovative companies come offering consumers the ability to divide small and medium-sized purchases into a set of manageable zero-interest installment payments while taking possession of the merchandise immediately.

The timing for these new services is the product of another major trend in payments—the death of the credit card.

Adoption rates for credit cards are falling off among younger Americans; only 33 percent of 18- to 29-year-olds according to one recent study have one. Many experts attribute this trend to the 2008 global financial crisis, which hit many Millennials just as they were transitioning into adulthood. It’s a generation that saw up close the impact of being over-leveraged and spending beyond one’s means.

This up-and-coming segment of the payment industry is in such a nascent stage that it still has trouble defining what to call itself. Whereas the moniker “post-pay” has gained some traction, others call it “buy now, pay later,” “digital layaway,” “deferred payments,” and “installment payments platforms.” Perhaps like Google, which won the war for search, the post-pay industry will someday be described by the name of the company that ends up leading the sector.

Regardless of how the industry ultimately decides to describe itself, the one thing that is pellucidly clear is this: four out of five Americans live paycheck to paycheck, and in that light, these deferred payment platforms are not only providing a compelling service, but filling a critical need in the marketplace.

The big names in this sector are probably unfamiliar to most Americans with names like Affirm, Afterpay, Klarna, SplitIt and Sezzle, but many industry experts posit that some of these companies could likely emerge as the Visas and Mastercards of the future, responsible for a significant portion of all online transactions both in the U.S. and globally. The leader in Europe is a Swedish venture called Klarna, while the company considered to be leading the revolution in the U.S. payment industry is Minneapolis-based Sezzle, which in less than two years signed up over 3,300 merchants and has just announced its expansion into Canada in a partnership with retailing giant Kappa Sportswear.

What Is Post-Pay?

Around the globe consumers from Brazil to South Africa to Australia—places that historically had weak credit markets—are intimately familiar with payment options that enable the consumer to pay for an item over a short period of time at zero interest. Payment arrangements such as these have been around for decades prior to the shift to e-commerce.

Here’s how layaway and other similar programs generally work: Sometimes the store holds the merchandise for the customer until all the payments are made in full; in other situations, particularly in places like Brazil with more advanced and integrated banking and financial systems, the retailer lets a customer take possession of the item on sight, but not before she leaves a stack of post-dated and signed checks with the merchant that will be scheduled to be cashed every month until the balance is paid off.

In the United States, the surge of online ‘alternative payment’ platforms—particularly those that focus on zero-interest payments made over a series of monthly installment—are popping up at checkout windows across the internet; yet for many U.S. shoppers, the idea is still viewed as something of a novelty.

“I suspect that deferred payment platforms, although they are quite new in the U.S. market, will expand rapidly and be increasingly visible on merchants’ online stores,” said Corey Davis, managing director of financial technology investment banking at BTIG. “Although the merchant will generally pay a higher fee to an alternative payment platform than is typical for credit cards, the growth in basket size and the ability to move more inventory at full price more than makes up for this added expense; retailers would rather sell merchandise now than have to unload it in three or four months at 50 percent off. The math is very compelling.”

Americans used to be very familiar with the layaway concept, which really took hold during the Great Depression as a means for families to get through during tough times. Like it was during the 1930s, today’s rise in popularity of companies like Klarna, Afterpay and Sezzle is coming once again as America is going through a phase of credit adversity. Although today’s online post-pay arrangements share their DNA with the layaway programs of the past, the array of offerings available to today’s savvy online shoppers are a far cry from corner retailer’s marketing tactics.

Sezzle Is the One to Watch

To be sure, none of the players in the deferred payments space are non-profits, yet Sezzle is becoming something of a merchant and consumer favorite, because of its utter simplicity; it’s one product—not an overwhelming menu of payment options, each with its own fine print. Unlike some of its competitors, like the embattled Afterpay which is now reeling over concerns from regulators about the company’s compliance with anti-money laundering and terrorism-financing laws, Sezzle strives to be, according to its own marketing material, “awkwardly transparent” about how it makes its money.

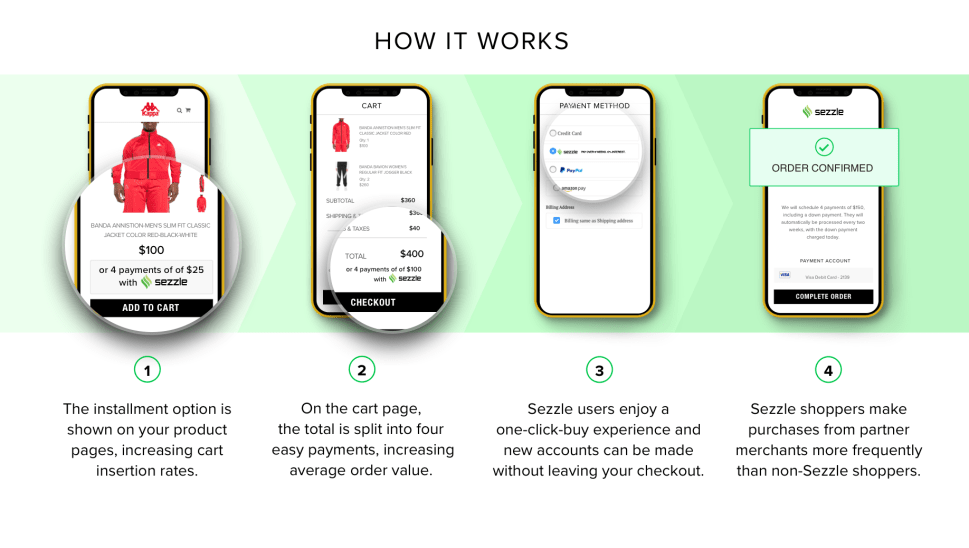

Here is how it works: Merchants pay Sezzle a processing fee—typically six percent of the purchase price—that, though higher than the fee merchants are charged for credit card processing, enable customers to expand their purchasing power by driving incremental sales, generating higher basket sizes, acquiring new customers and delivering more conversions.

Sezzle’s CEO and co-founder, Charlie Youakim, routinely says he wants customers to know how they make money and demystify the payment experience. This contrasts with companies like PayPal, which are often criticized by customers for dealing with shoppers in a less than transparent manner as they lock their talons into consumers’ banking and credit card information.

But it’s the customers who are the real winners with Sezzle, because they can acquire items they need now, but pay over time, without incurring a major hit to their credit or derailing their monthly budget. The only fees that Sezzle charges the shopper is in the case of failed or rescheduled payments, and Sezzle sends text and email reminders to customers to prevent late charges from occurring.

“Make no mistake about it, Sezzle is the way to pay for the bottom 99 percent of America,” observed Ethan Bearman, an analyst at FOX Business Network. “We all have experienced times when we need something now, but we don’t necessarily want to ring up a large tab on our credit card. Maybe the card is already maxed out, or maybe, as is the case with many younger Americans who saw what happened to their parents who spent their adult lives saddled with high-interest credit card debt, they are just fine ‘leaving home without it.'”

The Sezzle platform is open to anyone, but the company has clearly set its sights on younger consumers—Millennials and Generation Z.

Afterpay, on the other hand, despite its current woes with international authorities, is an Australian-based company that has been operating in the U.S. since early 2018; it offers consumers the ability to divide purchases into installments at zero percent interest. The knock against Afterpay has been its aggressive—some might say egregious—approach to late charges. Last year, a full 24 percent of the company’s revenue came from late fees. Nonetheless, Afterpay has rapidly become a major payment trend in Australia and the United States. Experts think Afterpay will be around for some time, but it has to catch up to Sezzle’s consumer-friendly focus and simplicity.

Klarna, a Swedish company (‘klarna’ means ‘clear’ in Swedish) is the dominant player in Europe and has been operating in the U.S. for a number of years. In Europe, the company works with some of the top retail brands such as Adidas, H&M, IKEA, Zara, Wish.com and Sephora. The company offers installments payments that charge interest, installment payments with no interest, and a “try before you buy” solution; the products available vary depending on the merchant and shopper, but one of the reasons Klarna has stumbled a bit in the U.S. is that it has changed the names and terms of its products so often that it has caused some confusion with consumers, which is reflected in poor customer review scores. Perhaps more problematic is that, unlike Afterpay and Sezzle, Klarna charges consumers on some products a high APR, which makes it less of a post-pay option than a credit product that can negatively impact a consumers’ credit score.

Another firm that has had some early success is San Francisco-based Affirm (AFRM), a point-of-sale loan provider. Affirm was one of the early entrants in the industry, focusing primarily on larger ticket items over $1,000, such as mattresses and furniture. Affirm only allows debit and check payment methods for their loans but does allow costumers to pay early with no fees or penalties; those who do not pay on time with Affirm can have their credit score negatively impacted.

Other players around the globe with different variations of the post-pay product include PayBright, Zip and QuadPay, in addition to a number of large retailers experimenting with their own proprietary solutions.

“The ‘buy now pay later’ payments model is really taking off in the U.S., and although some large retailers may experiment with their own solutions, at the end of the day, just like people don’t want to have a specific credit card for every store where they shop, we think that consumers will naturally gravitate to one or two alternative payments platforms that will be widely accepted across the entire online marketplace,” said Sezzle’s Youakim. “We believe that our company is well-positioned to be the ubiquitous ‘pay-in-installments’ solution for all of retail.”

For merchants, the advent of post-pay solutions is becoming a boon for sales.

“Shoppers from all around the world are becoming more in tune with the flexibility of technology, and are looking for that next best solution” observed Puneet Girdhar, the CEO of Kappa Canada which is partnering with Sezzle as the payment disruptor embarks upon its first foray outside the U.S. market. “Sezzle allows our shoppers to have freedom in what and how they purchase. We always want to make sure our customers are feeling confident and excited while shopping with us, without any hesitation.”

“The credit industry is basically built on misbehavior and profiting from consumers not paying on time—incentives are not aligned and we must change this paradigm,” Klarna CEO Sebastian Siemiatkowski told Observer. “Customers are smart, they are looking for a different and better way to pay.”

And with a half-trillion dollar market that is expected to double at stake, post-pay is one trend consumers will want to keep their eye on.