Payment Gateway Providers 101 – Why and How They Matter in Online Payment Processing

18 MIN READ

|

Updated on November 24, 2022

Summary: Payment gateways play a pivotal role in the online payment ecosystem, and using the wrong gateway to accept payments from your customers can send your entire payment process on a downward spiral. Picking a payment gateway that suits your business deserves more attention. Learn how and why payment gateway providers play an integral role in making your cash-registers ring, and how you, as a merchant can help in it. (Psst! We’ve created a neat payment gateway evaluator tool to assist you as well.)

The world thrives on networks. And networks thrive on connections. And connections thrive because of middlemen.

In The Middleman Economy, Marina Krakovsky makes a case for why this under-appreciated function is more ubiquitous and indispensable than we realize. The internet, for instance, was lauded as the “universal middleman,” by Bill Gates in one of his bestsellers.

One of the middlemen I interviewed, the micro-VC Mike Maples, Jr., put it well when he pointed out that in our highly connected world, “things and entities that accelerate connections are going to be more valuable.” This is why Maples is bullish on so many Internet businesses, having made early investments in Twitter, Lyft, and TaskRabbit, among others. “That’s what a middleman does,” Maples says: “They connect nodes in a network to increase the value of the network.”

And in this post, we’ll be focusing on one particular middleman in the online payment industry, who has been tirelessly working behind the scenes to connect the buyer and the seller and facilitate transactions between them.

Online transactions demand security. Reliability. Dependability. And a payment gateway takes it upon itself to provide you with all that.

Let’s see how it pulls it off, and what your role, as a merchant (business owner) is, in the online payment network.

From a bird’s-eye view, in an online transaction, a customer sends money from their bank account to the online payment ecosystem, which then passes on the money to the seller’s bank account.

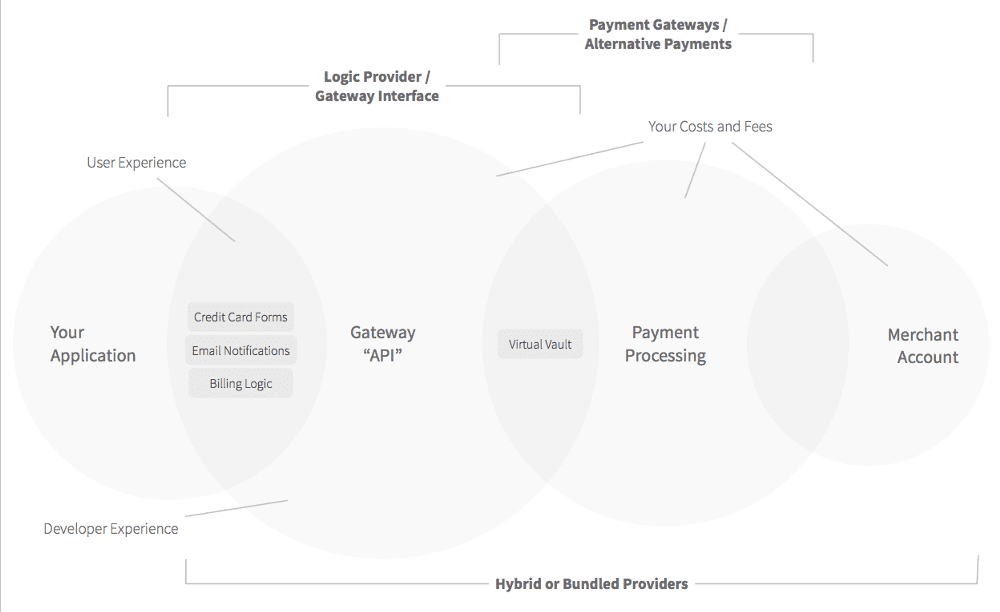

And the online payment ecosystem can be divided into three major clusters:

Consider them as the sub-middlemen between you (the seller) and the payment gateway provider, linking both of you via API. They come in at different points of your billing logic, like sending payment notifications, handling checkout pages, managing your subscriptions, functioning as your virtual vault, etc.

These function as the main middlemen in the network and work with your merchant account (Tl;dr – a special bank account that a merchant will need to accept card payments) to enable you to charge your customers.

Related Read: Credit Card Merchant Services vs. Payment Gateways

As the name implies, hybrids are a blend of logic providers and payment gateways, and make your billing job that much simpler. Think Stripe or PayPal. However, the catch here is that if you’re going to go with a hybrid, you might lose out on the flexibility to pick your payment gateway(s) or merchant account(s).

(Heads-up: Hybrids are the new black, and it won’t take too long for them to take over the payment gateway scene. So we’ll be looking from the hybrids context for the rest of the post, for the sake of clarity. We’ll also be predominantly focussing on card payments while talking about the online payment process, as it is the most widely-used and most elaborate process of them all.)

In order to elucidate the role of middlemen, Krakovsky breaks down their six prominent roles, which fits the payment gateway context like a glove:

Think of Uber. Or eBay. Or Kickstarter. They solely exist to bridge the passenger with the taxi, the seller with the buyer, and the maker with the investor.

A payment gateway provider falls bang in the middle of the payment processing system. It connects the buyer’s bank, the seller’s bank, the acquiring bank, and the issuing bank (bear with me on the jargons for now. By the end of this post, you’ll have befriended them all), irrespective of their physical, social, or temporal distance.

A headhunter is solely responsible for the quality of the candidates that she brings forth to the hiring table. Her reputation is on the line, and one bad apple can jeopardize her career. She has to vet each and every application thoroughly and must see to it that she only sends the best ones to the client.

Once a customer enters their card details, the payment gateway authenticates the card information, looks out for loose ends (if any), and gives a thumbs-up for the rest of the proceedings. In addition to this, a gateway also screens customer orders using an arsenal of anti-fraud tools, to well, prevent fraudulent activities.

An event planner’s job doesn’t end with connecting the clients with the vendors and service providers. She takes it upon herself to make sure that the clients receive the best service, that the vendors stick to their deadlines, and that the event takes place as smoothly as silk.

The payment gateway provider sees to it that the customer enters valid payment-related information, that the issuing bank authorizes the transaction after verifying the customer’s credit/debit limit, that the acquiring bank transfers the right amount to the seller’s bank account. It assures the customer and the business that the right amount of money is moved from the right place to the right place at the right time.

Insurance companies charge their customers for bearing and minimizing risk. And they manage the risk by spreading out investments into diversified portfolios.

Security is one of the core components of payment gateways, which encrypt and tokenize sensitive information like credit card numbers, use HTTPS protocol to communicate data, and comply with security standards like the Payment Card Data Security Standard (PCI DSS – we’ll be going through this in detail a bit later).

You can either choose to take the difficult route of researching and coming up with your own itinerary for your vacation to a foreign country, or hire a travel agent who can set it up for you in no time, thanks to their domain expertise.

Payment gateway providers make online payments a breeze for both the buyer as well as the seller even if they’re on the opposite sides of the world, by reducing (if not eliminating) security risks and manual intervention, and bringing the processing time of online transactions down to a few seconds. Thanks to payment gateways, the seller will be able to find the funds in his account in just a couple of business days, with little to no effort from her side.

By bringing themselves in between the two concerned parties, lawyers improve the quality of communication between them, enable strategic interactions, and help them in reaching a consensus faster.

You might be having the most sophisticated billing logic and an impeccable checkout experience in place for your customers. And in spite of all that, you will invariably reach a point where you’ll have no other option but to bring in a payment gateway in between you and your customer to complete a transaction. Why? Because it’s a much wiser trade-off to make, instead of spending your resources to meet the requirements of PCI DSS compliance (again, put a pin on this one. We’ve got a different section to talk about this). Think about it: would you rather toil on ensuring that your servers never get to touch your customers’ card details and storing your payment data, or just send the details over to a gateway that will securely handle them for you so that you can focus on perfecting your core product?

Summing it up, a payment gateway provider plays a predominant role in three activities:

Let’s see how this plays out in detail.

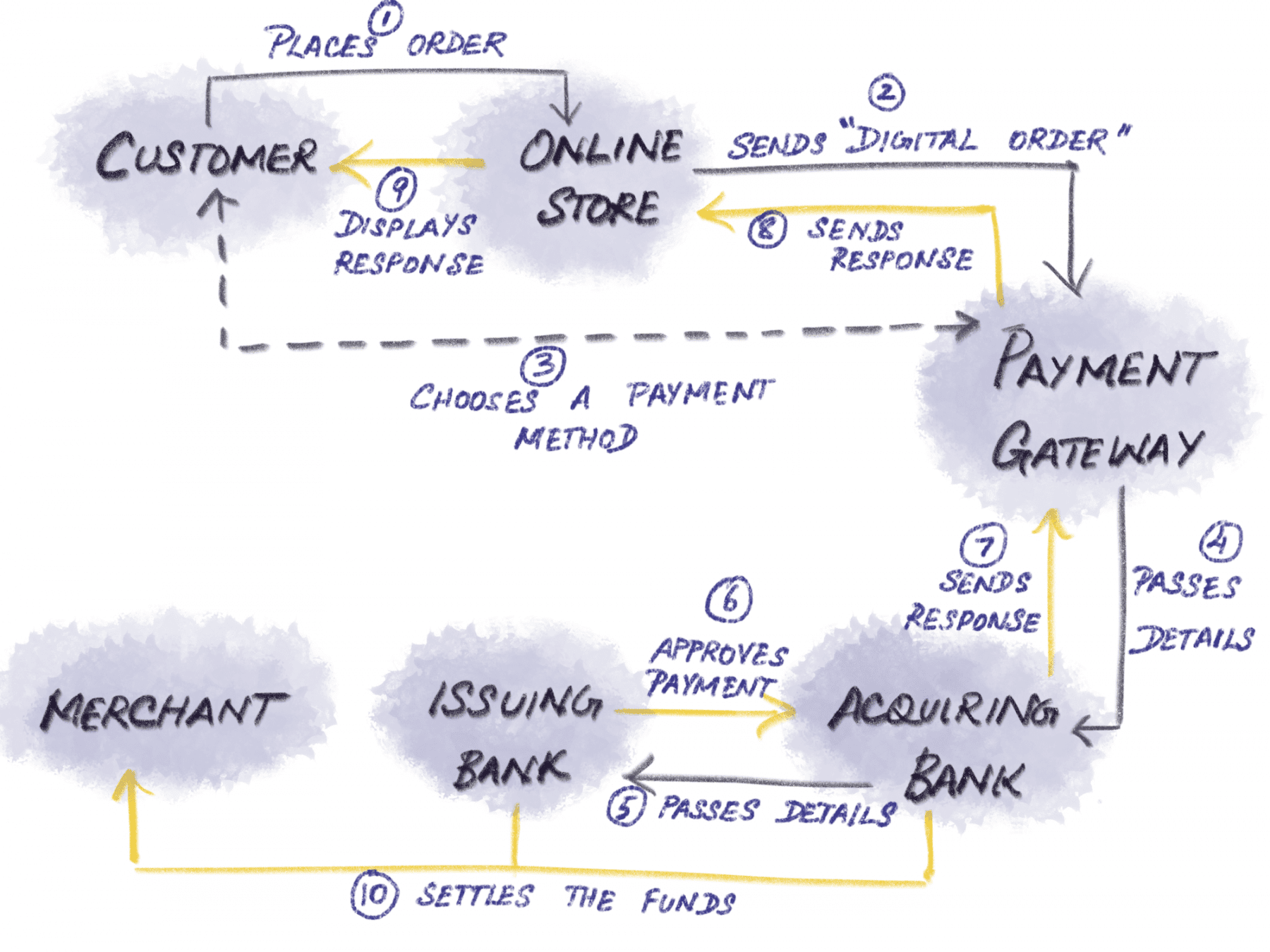

For a conventional online transaction to come through, you’ll need the following participants to work together (Warning – Jargon Alert! But fear not, I’ve tried my best to save you from acute jargon overdose):

Now that we’ve met the characters, moving on to the typical sequence of events:

And the best part? this entire process (from 1 to 8) takes up to 2-3 seconds at the most.

The final step (in the case of card payments) is for the issuing bank to “Clear” the Auth and settle the funds with the acquiring bank (in the case of physical goods, this step takes place after the merchant ships the order, i.e., fulfills the transaction).

Usually, at the end of the day, the merchant submits that day’s batch of all the approved Auths to the acquiring bank, which then requests the issuing bank for batch settlement. Once it receives the funds from the issuing bank, the acquiring bank, in turn, transfers the amount to the merchant’s bank account.

This period (from Authorization to settlement) is called the settlement time and is usually completed in anywhere from 2 to 4 business days.

You just need three reasons to get convinced. (Not-so-relevant plug: Behold the third three-pointer in this post. Sorry, I just had to note that down. Because, patterns.)

1. Enforcement – A payment gateway provider ensures that payment processing is secure and brings down the frequency as well as the severity of credit card frauds, with the help of these:

2. Ease – The present-day payment gateway providers can be set up in less than a day, and maintaining it demands minimal effort from your side. Most users have already interacted with payment gateways in their previous online shopping experiences, and so you needn’t put in the effort to get them familiar with how it works. In addition to that, most present-day payment gateways support multiple currencies and offer multiple payment methods, which takes a huge load off your shoulders to meet your individual customer needs.

3. Experience – Building on the previous sentence, by catering to the payment preferences of your global customers, you end up upping their satisfaction, and in turn your conversion rates. A survey conducted by YouGov discovered that about 50% online shoppers said that they would abandon their checkout process if their preferred payment method isn’t available. And that’s a lot of money left on the table.

There. If you can see a halo around “Payment Gateway” at this point, then we’re on the same page and can move on to the next (and final) section.

Now, no two payment gateway providers are the same, and each one comes with their own set of pros and cons. Which will vary depending on the type of your business and your location.

There are plenty of gateways in the sea, and no one gateway fits all.

Picking your payment gateway provider won’t be an ordeal by fire, if you know what factors to look for, and how to look for them.

As a good starting point, use this quick list of criteria (also, divided into three groups, wink wink, nudge nudge!) to evaluate payment gateways.

(Note: Apart from these, it does help to verify, as early as possible, if you run a high-risk business or sell a high-risk product, as it will affect your chances of receiving support from most payment gateway providers.)

The shortest distance between two points is not a straight line—it’s a middleman. And the more middlemen, the shorter.

“Good middlemen,” Marina Krakovsky says, “enlarge the size of the pie, making all parties better off.”

And it all starts with discovering and joining hands with the middlemen that are right for you and your business.

As a fellow startup in the trenches, we know how difficult a task it is to compare, weigh up, and pick out the payment gateway provider that will best suit your business.

That’s why we decided to do all the heavy lifting, and have come up with, drum rolls please, this nifty payment gateway comparison tool to help you evaluate payment gateway providerss specific to your country.

May your metaphorical cash-registers ring loud and long!