The Grattan Institute has released another excellent report entitled Hot property: negative gearing and capital gains tax, which completely demolishes the Turnbull Government’s scare campaign over Labor’s proposed changes to the negative gearing and the capital gains tax (CGT) discount.

Below is the Overview along with the key chart and tables:

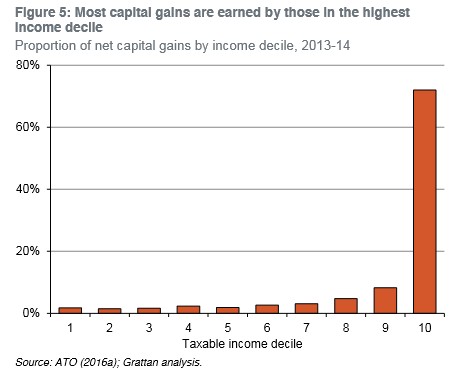

A substantial change to Australia’s tax arrangements is long overdue. The interaction of a fifty per cent capital gains tax (CGT) discount with negative gearing distorts investment decisions, makes housing markets more volatile and reduces home ownership. Like most tax concessions, these tax breaks largely benefit the wealthy.

These two measures in combination allow investors to reduce and defer personal income tax, at an annual cost of $11 billion to the public purse. Our proposals to wind back the discount and negative gearing would increase Commonwealth Government tax revenue by about $5.3 billion a year.

The discount on capital gains tax is designed to maintain incentives to save and invest. If income taxes are applied to nominal capital gains, inflation can erode part of an investor’s wealth. But given actual returns, and the CGT discount, many investors have been overcompensated for inflation.

Policy has overzealously protected savings at the expense of competing considerations. The economic benefits of tax neutrality for savings are small: those with high incomes save almost the same amount regardless of the tax rate. Providing a discount means that other taxes must be higher, and they impose greater economic costs. The 50 per cent CGT discount also encourages investors to focus too much on investments with capital growth rather than annual income. And it undermines income tax integrity by creating opportunities for artificial transactions to reduce tax.

Reducing the capital gains discount to 25 per cent would provide a better balance between these competing considerations and would raise about $3.7 billion a year.

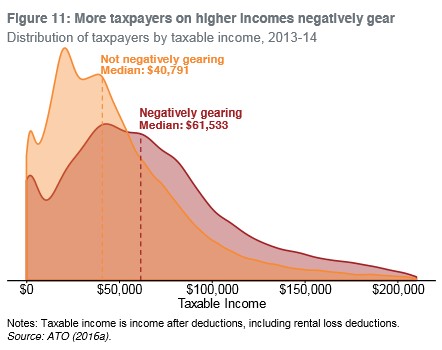

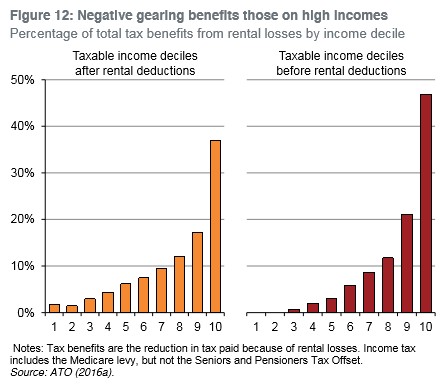

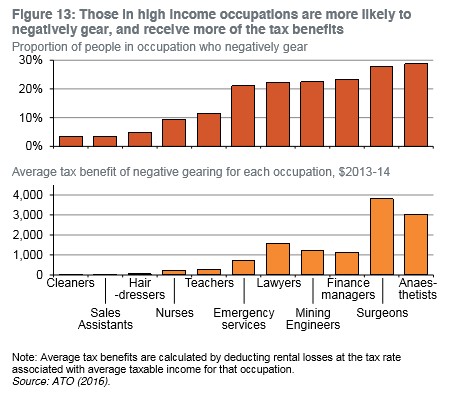

Negative gearing allows those who borrow to invest to use losses to reduce tax on wages and salaries. In Australia negative gearing goes beyond broadly accepted principles for offsetting losses against gains. It diverts capital from more productive investments without greatly increasing housing supply. Like the CGT discount, negative gearing primarily benefits those on high incomes.

Australia should follow international practice, and not deduct losses from passive investments from labour income. Change would raise $2 billion a year in the short term, falling to $1.6 billion as losses start to be written off against positive investment income. While other proposals, such as restricting negative gearing to new properties or limiting the dollar value of deductions, would improve the current regime, they nevertheless leave too many problems in place and introduce unnecessary distortions.

Our proposed changes will improve housing affordability – a little. We estimate prices would be up to 2 per cent lower than otherwise. Rents won’t change much, nor will the rate of new development. With tight constraints on supply of land suitable for urban housing, most of the impact will be felt via lower land prices. The changes will not cause housing markets to collapse: their effects on prices are small compared to factors such as interest rates and supply of land.

Phasing in change would reduce price shocks and make the reforms easier to sell. It is better than grandfathering current holdings, which would increase complexity, limit the additional tax collected for many years, and be unfair to new investors, especially younger ones.

Recommendations:

1. Reduce the capital gains tax discount for individuals and trusts to 25 per cent

x Phase in a 25 per cent discount over five years through reducing the value of the CGT discount by 5 percentage points each year.

2. Limit negative gearing. Quarantine passive investment losses so they can only be written off against other investment income

x Do not allow losses on passive investments to be written off against unrelated labour (wage and salary) income. x Allow losses on passive investment to be written off against all current year and future positive investment income, including interest, rental income and capital gains.

x Continue to allow losses from unincorporated business – sole traders and partnerships – to be written off against wage and salary income, subject to current restrictions.

x Do not create other exceptions such as allowing the write-off of losses up to a limit, on one or two properties, or on new properties.

x Phase in over five years by reducing the proportion of losses that can be written off against wage and salary by twenty percentage points each year.

3. In the longer term, aim to align the tax treatment across different types of savings

x Reduce taxes on other savings income such as net rental income and bank deposits so as to align with the tax treatment of capital gains. x Reduce and target the tax incentives for superannuation in line with the recommendations in Grattan’s Super tax targeting report.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.