There’s a growing segment of the American population that earns a decent salary but lives paycheck-to-paycheck: the income-rich and asset-poor.

Empty bank balances are often associated with those on the lowest rungs of the income ladder. But many members of America’s upper-middle class have almost no emergency cushion and are woefully unprepared for retirement. And years into the recovery, they are still struggling, leaving the entire economy vulnerable.

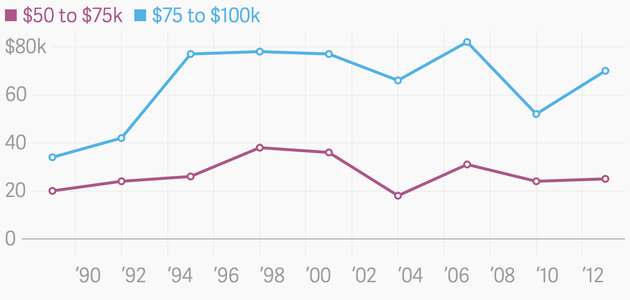

The median household income in America is about $55,000. To earn more than that is to do relatively well, particularly in low-cost areas. That’s what they bring in, but what do they really have? The figure below plots financial assets held by members of the upper-middle class aged 40 to 55. (Financial assets are any assets a household owns that isn’t a house, car, or business, which means it includes all retirement funds.)

Average Value of Household Assets, by Household Income

Quartz | Data: Federal Reserve

Even a relatively high earner who has been working many years typically only has $70,000 in financial assets, which isn’t even a year’s salary for a high earner. That’s just the average—about 25 percent of upper-middle-class 40- to 55-year-olds have less than $17,500 in financial assets. Financial assets trended up in the 1990s, and have nearly recovered since the financial crisis. But one reason asset balances went up is the increased popularity of 401(k) plans. In the 1980s, companies saved for their employees through defined-benefit pensions. Now, people do it for themselves.

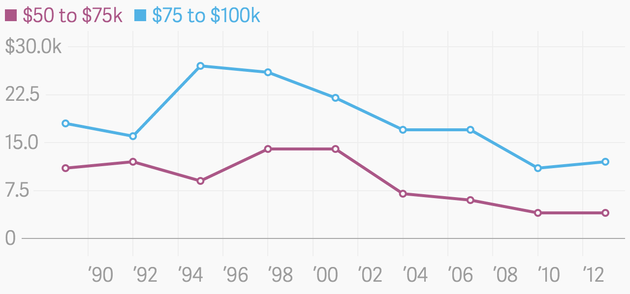

The figure below represents financial assets without retirement accounts. And it looks like the upper-middle class has fewer assets than ever.

Average Value of Household Assets (Excluding Retirement Accounts), by Household Income

Quartz | Data: Federal Reserve

Of course, 401(k) savings probably displaced other forms of saving. That is, after putting money into their retirement accounts, people don’t have much left over to save in other ways or don’t feel the need to do so. But this could also lead people to rely on those accounts in a pinch, which is a bad strategy since retirement accounts have penalties for early withdrawal. The fact that the average upper-middle-class household has just $12,200 in non-pension financial wealth is disturbing. Even worse, within that group, about 25 percent of the higher-earning population had only $3,200 in 2013. It’s no wonder one-quarter of all American households couldn’t come up with $2,000 if they faced an emergency—it’s not just low earners.

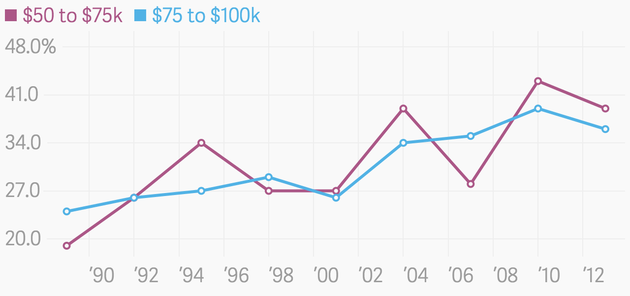

The financial picture gets even darker when factoring in how much debt the upper-middle class has. Below is the leverage ratio (similar to how people assess bank health), which represents how much debt someone has relative to their assets.

The Ratio of Debt to Value of Household Assets, by Household Income

Quartz | Data: Survey of Consumer Finances

The majority of this debt is related to housing, and, increasingly, student loans. In terms of assets, most wealth remains tied up in real estate. As the housing crisis proved, that’s a risky proposition for those without much in liquid savings. After getting laid off, there’s no cushion to ensure people can still pay their mortgages.

It’s common to say that the U.S. economy relies on consumer spending to keep it humming. That thinking justifies high levels of household debt as a trade-off for a booming economy. But that’s wrong. Consumer spending isn’t what makes a healthy economy; it’s people building and creating things. To support those activities, consumer spending needs to be stable and predictable.

The problem with having no savings is that when something goes wrong, or workers retire, they suddenly need to cut back. If that happens, it’s painful not only for those individual households, but the broader economy. So it’s not just low earners who are vulnerable.